The end of last week on global stock markets could only be described as euphoric. The two main US indices – the S&P 500 and the Nasdaq – climbed to all-time highs. Not only have they recovered from losses linked to the Iran conflict, they have moved beyond pre-crisis levels.

Disconnected from Reality: The Gas Paradox and Hormuz

Such growth would be justified if a credible peace agreement were in place, one that clearly defined the rules and ensured stability and economic confidence for years ahead. But no such agreement exists.

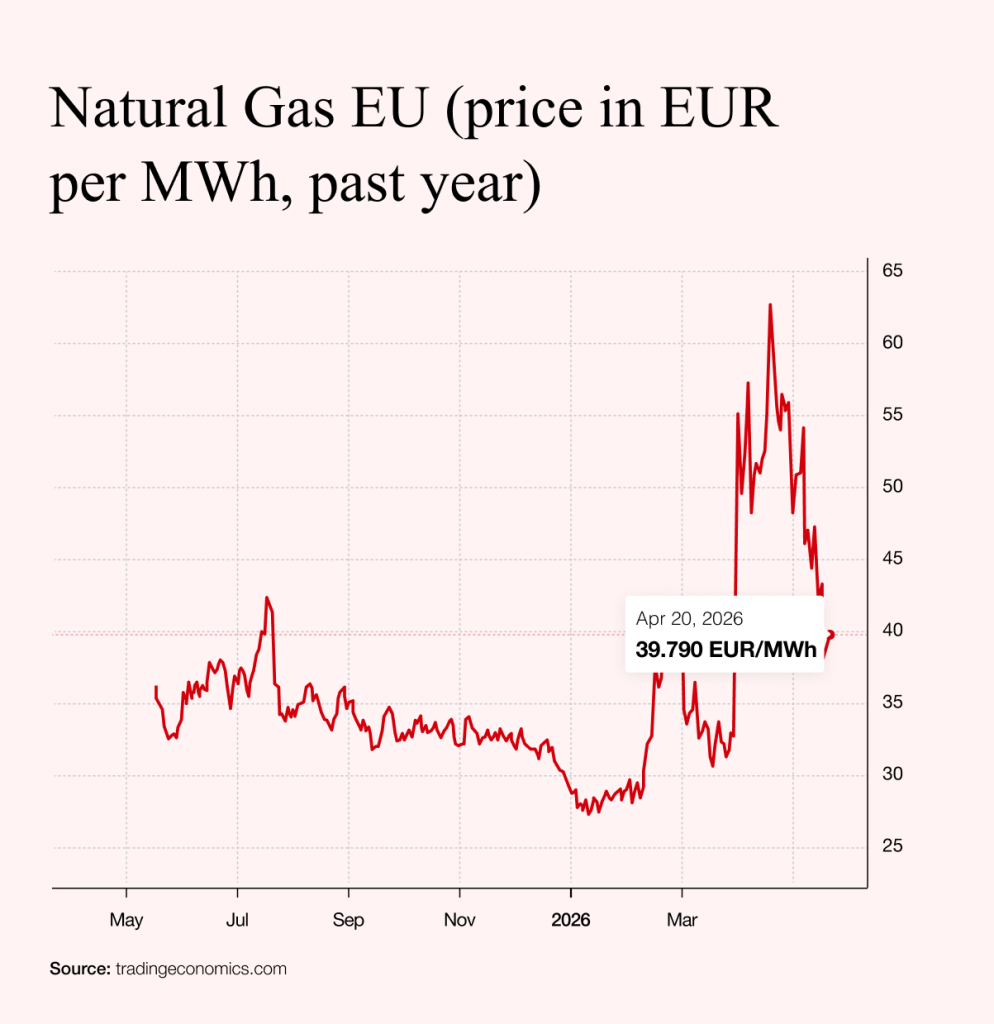

Oil prices have fallen by more than 10% on reports that the Strait of Hormuz remains open. Even more striking, however, is the decline in natural gas prices, which points to a growing disconnect between market behavior and underlying fundamentals in Europe.

Take storage levels. In the Czech Republic, for example, reserves fell to 21% after the winter, compared with 25% the previous year. A similar pattern can be observed across much of Europe.

More importantly, the refilling season officially began on 1 April. Last year, storage levels began to rise steadily during the month. This year, however, volumes only started to increase in the second half of April.

The explanation is straightforward. Buyers are reluctant to secure supplies at elevated prices, instead betting on a decline if the conflict subsides. The problem is timing. Even if tensions ease, it will take time for LNG shipments from the Gulf to reach Europe and Asia.

Summer is the critical period for replenishing reserves. With storage levels currently low, the market faces a potentially strained season. Gas prices have fallen so sharply that they are now below last year’s levels during a crucial refill window – a development that appears difficult to justify on fundamental grounds.

However, the narrative of an imminent end to the conflict was undermined over the weekend when Iran signalled it could close the Strait in response to the US blockade. As expected, oil prices rose on Monday morning, while gas – which had previously fallen sharply – also rebounded.

Investors are now faced with a familiar conundrum: how to navigate markets dominated by rapidly shifting headlines, where a single announcement can reverse price trends.

What, then, would constitute a reliable signal that the crisis is truly ending? The most telling indicator is hard data on shipping volumes through the Strait of Hormuz. Before the crisis, around 130 vessels passed through daily. Since then, activity has dropped sharply. The highest figure recorded was 19 ships on 15 April. Over the weekend, traffic fell to just five vessels, before rising slightly to eight on Monday.

In other words, the situation remains far from normal. Until volumes recover to at least 100 ships per day, it is difficult to argue that the crisis has meaningfully subsided.

The Return of TINA and Faith in Tech Giants

On US equity markets, investors appear to have returned to the TINA strategy – “There Is No Alternative”. The logic is simple: any sign of de-escalation in the Iran conflict is likely to drive further gains, making it attractive to concentrate on established leaders, particularly the so-called Magnificent Seven.

Attention has focused on companies that have underperformed in recent months, notably Microsoft and Meta.

These declines had clear underlying causes. Microsoft’s Copilot language model, despite heavy investment and early promise, has struggled to establish itself among the leading artificial intelligence tools.

Meta, meanwhile, faces ongoing legal risks and a persistent lack of diversification beyond its core advertising business. Yet these concerns appear to have been largely set aside, as investors return to both stocks in anticipation of renewed growth should diplomatic progress materialize.

In this environment, markets appear to respond more to signals from Washington than to Tehran’s more cautious stance.

Earnings Season and the Commission Effect

There is, however, a more conventional driver behind recent market strength: the first-quarter earnings season.

The reporting period has begun with US banks, where early results have been broadly positive. Of 65 institutions reporting so far, 45 have exceeded analysts’ expectations.

Bank of America and Morgan Stanley posted profit increases of 25% and 29% respectively, supporting their share prices. Citigroup reported a 42% rise in net income, benefiting from heightened market volatility.

Markets, however, have shown little tolerance for weaker performance. Wells Fargo reported higher profits, yet its shares fell by 5.6% following disappointing results. J.P. Morgan, meanwhile, saw limited upside, as strong performance had already been priced in.

At the same time, heightened market uncertainty has driven significant inflows into asset managers such as BlackRock. A closer look at bank earnings suggests that trading divisions delivered particularly strong results in the first quarter.

This does not imply access to privileged information. Rather, it highlights a structural advantage: in periods of volatility, professional investors are better positioned to generate returns.

For individual investors, geopolitical uncertainty may be a source of anxiety. For large financial institutions, it often represents opportunity.

In that sense, an old market truth holds once again: volatility rewards those who can manage it – and, in many cases, those who profit from facilitating it.