If US stock market indices were the only guide to geopolitics, a peace agreement might appear to have already been signed, with only a formal announcement pending. In reality, the S&P 500 has crossed 7,000 points for the first time.

Its value is now at an all-time high, despite oil prices stubbornly holding above $90 per barrel.

Around 20 ships now pass through the Strait of Hormuz despite the dual blockade. Normal operations, with around 100 vessels a day traversing the strait, appear to be a thing of the past.

Shipping data from Kpler show that between 28 February and 12 April, just 279 ships passed through the strait, well below the pre-war average. Although the US–Iran ceasefire came into force on 8 April, only 45 vessels have entered or exited the strait since then.

Markets remain undeterred by the sharp drop in traffic or elevated oil prices. Donald Trump continues to fuel expectations that Iran is eager to conclude a deal swiftly. So far, markets appear to accept that narrative. Yet investor sentiment alone does not explain the S&P’s record high.

Software Under Pressure

Since the beginning of the year, software developers have faced sustained pressure. The prevailing view has been that artificial intelligence, through its universal application, will soon enable individuals to develop applications and services tailored precisely to their needs.

While the notion that everyone will soon be programming their own applications in their spare time is clearly exaggerated, software stocks have repeatedly declined as news of advances in AI has accumulated.

The latest trigger was the announcement of a new model by Anthropic, aptly named Claude Mythos, which is expected to excel in identifying software security vulnerabilities. The news pushed the entire sector into the red, with shares falling by more than 7% over three days.

This week, however, brought an unexpected reversal. Analysts have reassessed their outlook, concluding that while AI will eventually replace traditional products, the transition will not happen overnight. Moreover, many of the companies affected are established firms that continue to generate strong profits and maintain high margins.

At the same time, companies are actively integrating AI into their ecosystems to remain competitive. Their position will not be easy, but they are likely to remain viable for several years. Given that valuations are currently low, they may even present attractive investment opportunities.

A sharp rebound followed. The technology sector rose by 5.4%, marking its strongest trading day since April 2025. Oracle gained 12.7%, ServiceNow rose 7.3%, CrowdStrike advanced 6.1% and Salesforce added 4.8%.

While the rally in technology stocks reinforces the impression that conditions are improving globally, this is largely illusory. Warning signs continue to accumulate.

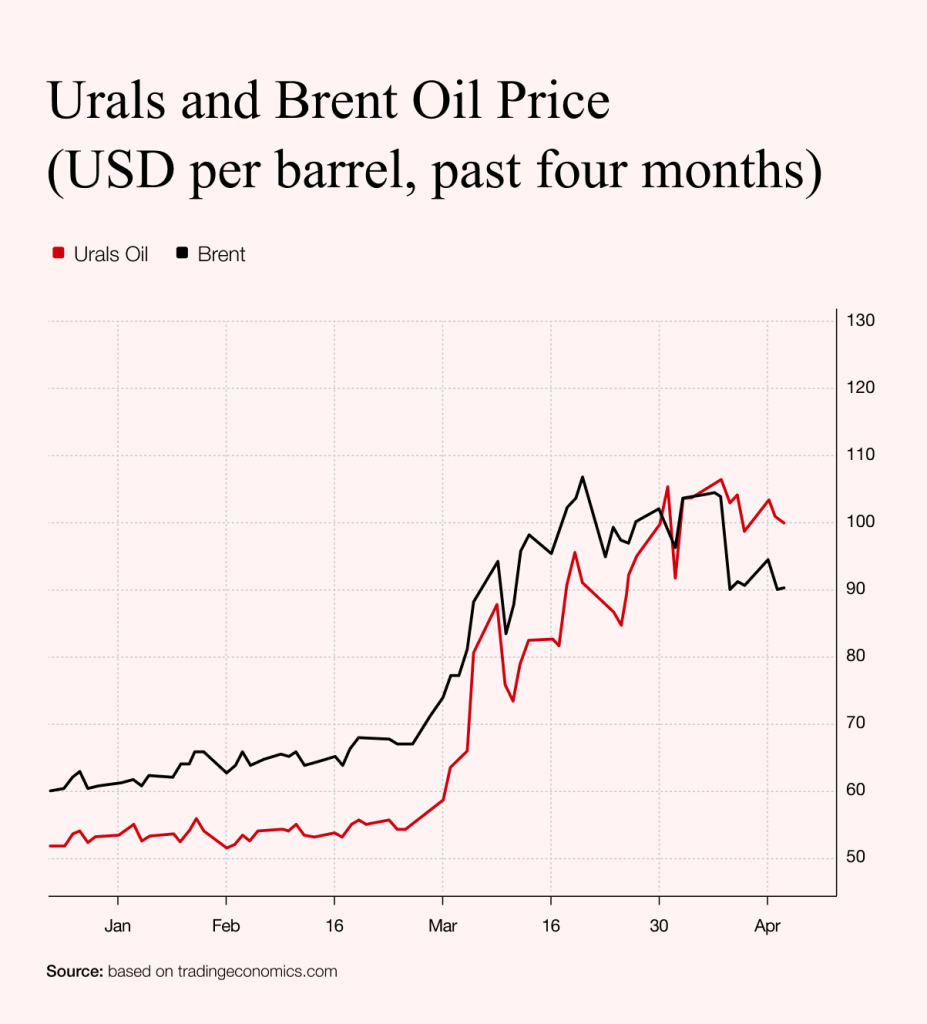

When Urals Beats Brent

For now, financial markets appear to have paused their earlier panic. Oil prices below $100 per barrel are seen as broadly reflecting the risks associated with the ongoing geopolitical conflict. High oil prices are not unprecedented, and economies have historically adapted. Inflation may be rising, but there is no immediate sense that it is spiralling out of control.

Markets remain dominated by optimists who believe that Donald Trump has the situation under control, will soon announce a major international agreement, that oil prices will subsequently fall and that his nominee at the Federal Reserve will sharply cut interest rates. Under such a scenario, US equities would experience another surge, and he would win the November election decisively. That is the ideal outcome envisioned by committed supporters. The difficulty is that each additional day of persistently high oil prices makes that trajectory harder to sustain.

This underlying tension is most clearly reflected in global oil price movements. It is not sufficient to examine a single benchmark; meaningful analysis requires comparison.

Since early April, a highly unusual development has emerged: Russian Urals crude has traded at a premium to North Sea Brent. Until recently, Urals crude was sold at a significant discount due to sanctions and its lower quality. The temporary easing of restrictions and a dramatic supply shortfall of 13 million barrels per day initially brought the two price benchmarks closer together. Now, however, Urals trades above Brent.

The explanation lies in the divergence between financial markets and physical supply. Brent prices largely reflect futures contracts and market expectations of a ceasefire and the reopening of Middle Eastern supply routes. By contrast, the elevated price of Urals crude reflects acute shortages in the physical market.

Asian refineries, particularly in China and India, have lost access to key supplies due to the disruption in the Strait of Hormuz. Russian crude, however, continues to reach them via routes that bypass the conflict zone. Energy-hungry economies require physical supply to sustain industrial activity and are therefore willing to pay a premium for available cargoes.

In April, established assumptions about oil quality and sanctions were effectively set aside. The premium shifted to crude that could be delivered reliably. The rise in Urals prices demonstrates that, despite record highs in equity markets, the global energy challenge remains unresolved. Buyers are clearly willing to pay significantly more than under normal conditions.

The Long Road Back

The prospect of a return to normal conditions in the oil market has so far received limited attention. Even if a US–Iran agreement were concluded immediately, restoring full operations in the Strait of Hormuz and resuming production and processing would take considerable time.

Insight can be gained from physical contracts for Omani crude, which are still trading above $101 for June delivery.

Here, too, physical oil commands a premium of more than $10 over exchange-traded prices. Market indicators suggest that oil prices may not fall below $80 before October 2028.

Although the Omani exchange is relatively illiquid, it offers a plausible indication that energy prices are likely to remain elevated in the months ahead. That fundamental reality is not reflected in current equity valuations.