In any tightly contested election, there is uncertainty before the vote count. Afterwards, however, the world is suddenly filled with experts who know exactly why things turned out the way they did. In the case of Hungary, one certainty existed long before the election weekend: Viktor Orban’s Achilles heel is the economy. After 16 years in government, it became increasingly clear that the promised Orban-style economic miracle would not materialize.

In recent years, Orban’s strategy has focused primarily on shifting attention to the international stage, building his foreign reputation and maintaining ties with the most powerful actors.

In the domestic economy, meanwhile, Fidesz rhetoric has been reduced to a fatalistic claim: nothing else can be done unless the state is willing to make brutal budget cuts that would be painfully felt by every Hungarian.

It was precisely this fear of belt-tightening that became the main driver of the campaign against Peter Magyar. The government machine persistently accused him of concealing his real plans behind a polished official program.

A Phantom Document and a Legacy of Mistrust

The culmination of these efforts to discredit Magyar’s economic intentions was the scandal surrounding an alleged 600-page internal document from the turn of 2025 and 2026. At the time, the pro-government portal Index claimed that the Tisza party was preparing a draconian fiscal package in absolute secrecy.

The document allegedly included measures toxic for Hungarian voters: the end of the flat tax and a return to progressive income taxation, a drastic reduction in family allowances and new across-the-board property taxes. According to media claims, the package would have taken thousands of billions of forints out of the pockets of households and companies. It was quickly labelled “Tisza-ado” (Tisza tax).

There was one major problem. The link between the document and Tisza was never confirmed, and a court later ruled that Index had falsely claimed the material originated in the party’s economic cabinet. The outlet was forced to publish a correction.

The real author of the document remains unknown. Nevertheless, the phantom plan served its purpose during the campaign. It allowed government-aligned media to reinforce the narrative that beneath the polished image of the new prime minister lay a radical experiment ready to undermine the Hungarian middle class.

This is the legacy of mistrust that the new government will have to confront quickly, both on financial markets and among its own voters. Above all, it will need to demonstrate that there is no hidden agenda and that its actions will be transparent.

An Economy on the Brink and a Depleted Treasury

The problem is that the Hungarian economy Magyar inherits is teetering on the edge. Macroeconomic data illustrate why Orban’s model has lost support. While Hungary experienced a strong post-pandemic rebound in 2021 and early 2022, the economy slipped into recession from late 2022 and has since endured prolonged stagnation.

In 2024 and 2025, quarterly GDP growth hovered close to zero and occasionally turned negative. The country is effectively stagnating.

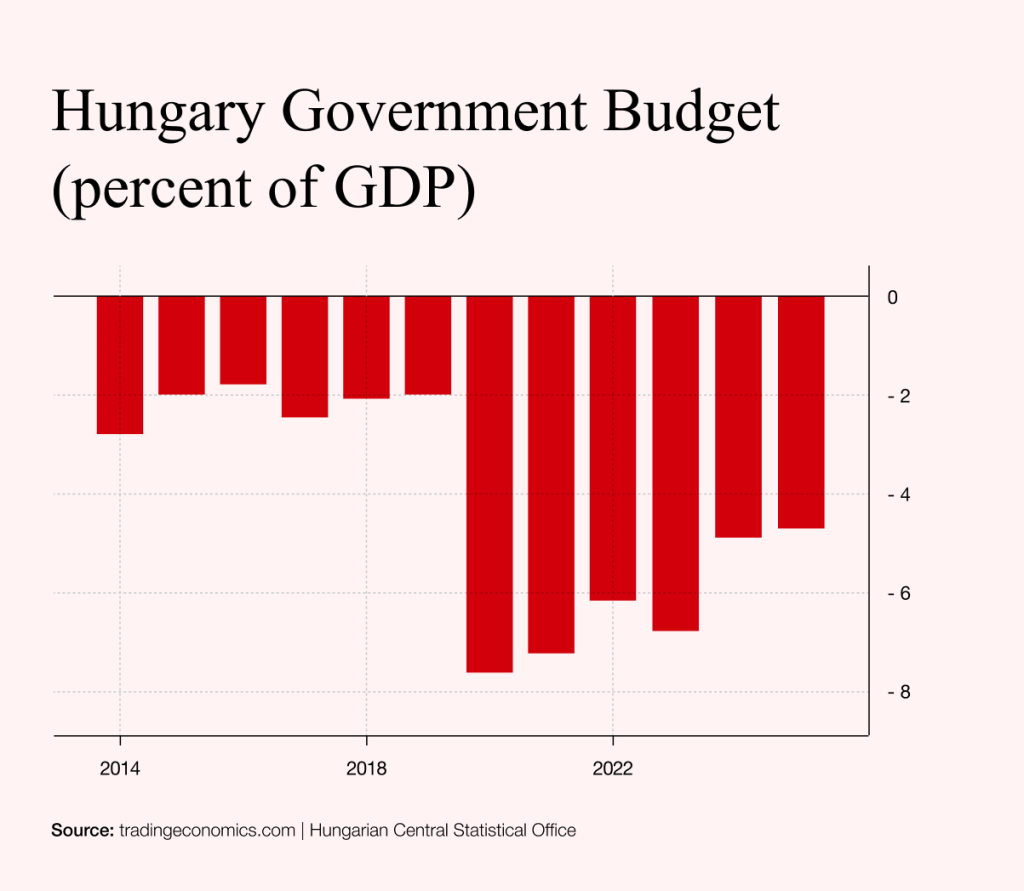

Even more concerning is the state of the public finances. Fidesz has hit the same fiscal ceiling that is weighing on other European governments, from France to the Czech Republic to Slovakia: the inability to return the budget deficit to pre-pandemic levels.

Hungary kept its deficit below the Maastricht threshold of 3% of GDP between 2014 and 2019. The pandemic shock pushed it to 8% in 2020, and it has not been brought back under control since. Even in the pre-election years of 2024 and 2025, the deficit remained between 4.5% and 5% of GDP.

The new prime minister is fully aware of this constraint. His program may be filled with costly social promises, but his overriding priority is to reduce the deficit from around 5% to the Maastricht benchmark of 3%.

For Magyar, this is essential. One of the key differences between him and Orban lies in his approach to adopting the euro, which he intends to complete by 2030. The question is how he plans to achieve this while insisting that ordinary citizens will not bear the cost. His strategy rests on four pillars: better use of European funds, a determined fight against corruption, renewed efforts to attract foreign investment and a reduction in debt-servicing costs.

A Bet on Brussels and a Hard Macroeconomic Limit

On paper, this appears to offer a painless solution, but it has a fundamental flaw. These are broad objectives that almost any government, including Orban’s, would endorse. Fidesz also sought to reduce debt costs and attract investment.

The challenge has never been identifying what needs to be done, but implementing it. Expecting a large fiscal gap to be closed solely through anti-corruption efforts is a common illusion among incoming governments.

Magyar’s main bet is therefore on the West, specifically Brussels. He is counting on the European Union to welcome Hungary back and to unblock frozen funds. Political willingness to do so may indeed be strong. Yet this approach will soon encounter a hard limit: Europe itself has little fiscal room to manoeuvre.

Germany’s industrial base, long the continent’s economic engine, is struggling with structural challenges. France, the bloc’s second-largest economy, is also facing mounting debt pressures.

Prospects from outside Europe are equally uncertain. Global investors increasingly direct capital towards the United States or Asia rather than a stagnant continent.

Orban has already turned to Chinese capital in recent years, partly because access to Western investment has narrowed. As a result, even if Magyar is warmly received in Western capitals, he may quickly discover that European resources are far from limitless.

If he does not want to return power to Orban within four years, he will need to find new sources of growth at home. Otherwise, he will have to take a deep breath and begin making the very unpopular decisions he claimed during the campaign did not exist.